Breeden–Litzenberger (BL)¶

Using the discovery endpoints discussed in the Workflow section, let's investigate some data from the Breeden-Litzenberger set.

# pip install matplotlib numpy

import matplotlib.pyplot as plt

from datetime import datetime, timezone

import numpy as np

# Breeden-Litzenberger.

metric = "bl"

# S&P 500 index.

ticker = "SPXW"

# 2026-01-30 21:00:00 UTC, CBOE closing time.

expiry = "1769806800"

# 2026-01-27 11:45:56 UTC

measurement_time = "1769514356"

# Get the data from Reflex Research.

data = get_measurement(

metric,

ticker,

expiry,

measurement_time,

)

# Visual check of data.

print(data)

# Quick check of some statistics.

x = np.asarray(data["payload"]["data"]["underlying"], dtype=float)

pdf = np.asarray(data["payload"]["data"]["pdf"], dtype=float)

# This should be very close to 1, as it represents a probability

# distribution.

area = np.trapz(pdf, x)

# Underlying price where the PDF is a maximum.

mode_x = x[np.argmax(pdf)]

# Standard deviation.

mean_x = np.trapz(x * pdf, x)

var_x = np.trapz((x - mean_x) ** 2 * pdf, x)

std_x = np.sqrt(var_x)

# Skewness.

skew_x = np.trapz(((x - mean_x) / std_x) ** 3 * pdf, x)

print("Area:", area)

print("Mode:", round(mode_x, 2))

print("Mean:", round(mean_x, 2))

print("STD:", round(std_x, 2))

print("Skew:", round(skew_x, 2))

# Get measurement time for display.

meas_dt = datetime.fromtimestamp(

data["measurement_time"], tz=timezone.utc

).strftime("%Y-%m-%d %H:%M:%S")

# Get expiry time for display.

exp_dt = datetime.fromtimestamp(

data["expiry"], tz=timezone.utc

).strftime("%Y-%m-%d %H:%M:%S")

plt.figure(figsize=(10, 6))

plt.plot(x, pdf, lw=2)

plt.xlabel("Underlying price")

plt.ylabel("Probability density")

plt.title(

"Breeden-Litzenberger Probability Density\n"

f"{data['ticker']} | Measured {meas_dt} UTC | Expiry {exp_dt} UTC"

)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

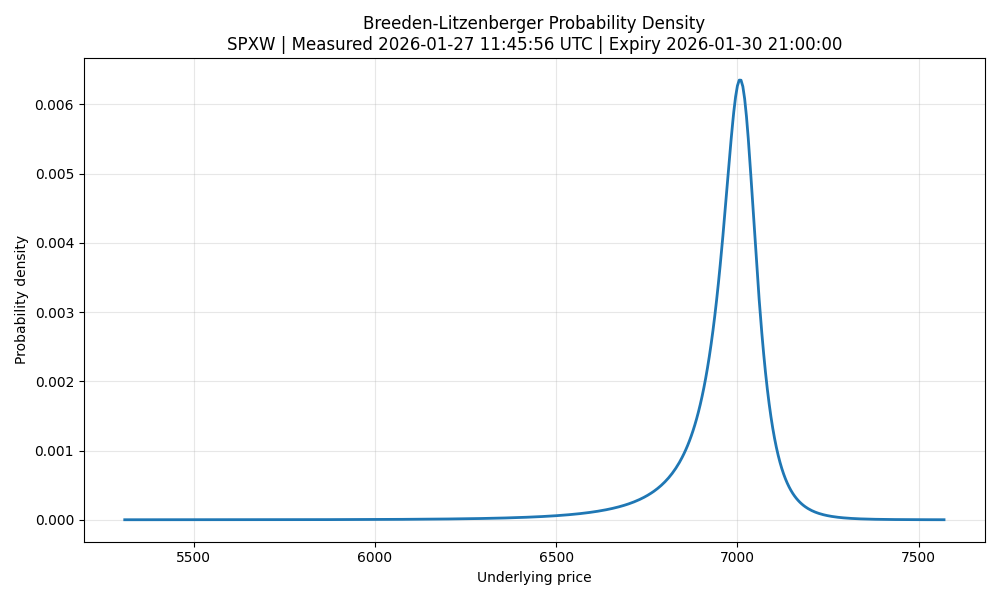

For this example, the following statistics were obtained:

This data gives some useful insights into what the market is pricing in, for the expected value of the S&P 500 at the end of the trading day of 2026-01-30. The negative skew indicates a fat tail distribution where downside risk is anticipated.

A plot of the data is shown below.